Quick Summary

U.S. markets finished the holiday-shortened week with a constructive but selective tone. The S&P 500 moved modestly higher, while the Nasdaq and QQQ showed stronger relative leadership as technology and semiconductor-related names rebounded into the end of the week.

The tone was not fully risk-on. A more hawkish Federal Reserve message kept rates and inflation risk in focus, while Canadian equities cooled after reaching a record high earlier in the week. The main takeaway is that leadership remained concentrated, macro sensitivity stayed elevated, and next week’s inflation and growth data could matter for short-term direction.

Market Tone

The market tone was mixed to constructive.

Technology leadership helped the U.S. market hold up, but the week also showed how quickly sentiment can change around Federal Reserve communication, bond yields, energy prices, and geopolitical headlines. Strength was visible in growth and semiconductor themes, while some defensive, commodity-linked, and rate-sensitive areas looked less consistent.

For Pragy Investments, this is a week where confirmation matters more than prediction. Strong groups can continue to lead, but the next macro data points may influence whether the move broadens or stays concentrated in a narrower set of names.

SPY / QQQ Context

SPY remained steady to modestly higher on the week, reflecting a market that is still supported but not broadly aggressive. The S&P 500 benefited from improving sentiment into the final U.S. trading session before the Juneteenth market closure.

QQQ showed stronger relative action than SPY. Mega-cap technology, software, and semiconductor-linked areas helped the Nasdaq regain momentum after midweek pressure. This keeps QQQ on the leadership side of the market, but the move still depends on whether technology breadth can hold and whether rate expectations stay contained.

A practical read is that SPY continues to represent the broader market’s resilience, while QQQ remains the higher-beta leadership gauge. If QQQ keeps leading while SPY holds its range, market tone can remain constructive. If QQQ leadership fades, broader index momentum may become more fragile.

TSX / Canadian Market Context

The TSX had a more cautious finish. Canada’s main index pulled back after reaching a record closing high earlier in the week, with weakness in materials and gold mining shares weighing on the index.

This matters because the Canadian market is more exposed to commodities, financials, and resource-linked rotation than the U.S. large-cap growth indexes. When gold, oil, or materials weaken, the TSX can lag even when U.S. technology remains firm.

The Canadian setup is still not broadly negative, but it is more selective. Financials, materials, energy, and domestic macro data remain important for reading whether TSX weakness is temporary consolidation or a deeper rotation away from recent leaders.

Strong Sectors

Technology and semiconductor-related groups showed the clearest strength. The rebound in chip-related names helped QQQ outperform and kept artificial intelligence, advanced computing, and infrastructure-linked technology themes in focus.

Technology services also remained important because software, cloud, cybersecurity, and data-center exposure continue to act as major watchlist areas when growth sentiment improves.

Manufacturing and industrial-linked themes stayed relevant, especially where companies are tied to automation, electrification, power infrastructure, reshoring, and productivity spending. These areas can participate when the market favors real-economy growth themes rather than only mega-cap technology.

Financials also remain worth monitoring. Higher-rate expectations can be mixed for the group, but banks and capital-market names may still show relative strength when credit stress stays contained and the broader economy avoids a sharp slowdown.

Weak Sectors

Materials and gold mining were weaker in Canada as gold prices pulled back and miners weighed on the TSX. This is a useful reminder that commodity-linked leadership can reverse quickly when the U.S. dollar, rates, or global risk sentiment shifts.

Energy was also less consistent. Oil-price volatility remains tied to geopolitical developments, supply expectations, inflation concerns, and central-bank interpretation. That makes the group important to watch, but not easy to read from one session alone.

Consumer-linked areas looked more selective. When inflation and rate expectations remain elevated, discretionary spending themes can face more scrutiny. Defensive consumer areas may also lag when market participants rotate back toward growth and technology.

Notable Watchlist Themes

AI and semiconductor infrastructure remained the most visible leadership theme. The focus is not only on chipmakers, but also on power infrastructure, cooling, data-center equipment, automation, and software platforms tied to AI demand.

Pullback setups in leading technology names remain worth observing, especially where price action is consolidating instead of breaking down. In a selective market, cleaner bases and higher-quality relative strength can matter more than chasing extended moves.

Canada materials and gold miners need confirmation before being treated as leadership again. The group can rebound quickly, but the week’s weakness shows that commodity themes remain sensitive to gold, the U.S. dollar, and rate expectations.

Financial and industrial names remain useful secondary watchlist areas. If the market broadens beyond technology, these groups may help confirm healthier participation. If they fail to follow through, leadership may stay narrow.

Risk Notes

Markets can change quickly around macro data, central-bank communication, bond yields, commodity prices, and geopolitical headlines.

Strong sectors can cool without much warning, especially after fast moves. Weak sectors can also rebound sharply when positioning, rates, or commodity prices shift. Watchlist ideas need confirmation through price action, volume, relative strength, and clearly defined invalidation levels.

Event risk is elevated next week because inflation and growth data are scheduled after a Fed meeting that already leaned more hawkish. The focus should remain on process, risk control, and avoiding overconfidence in any single market narrative.

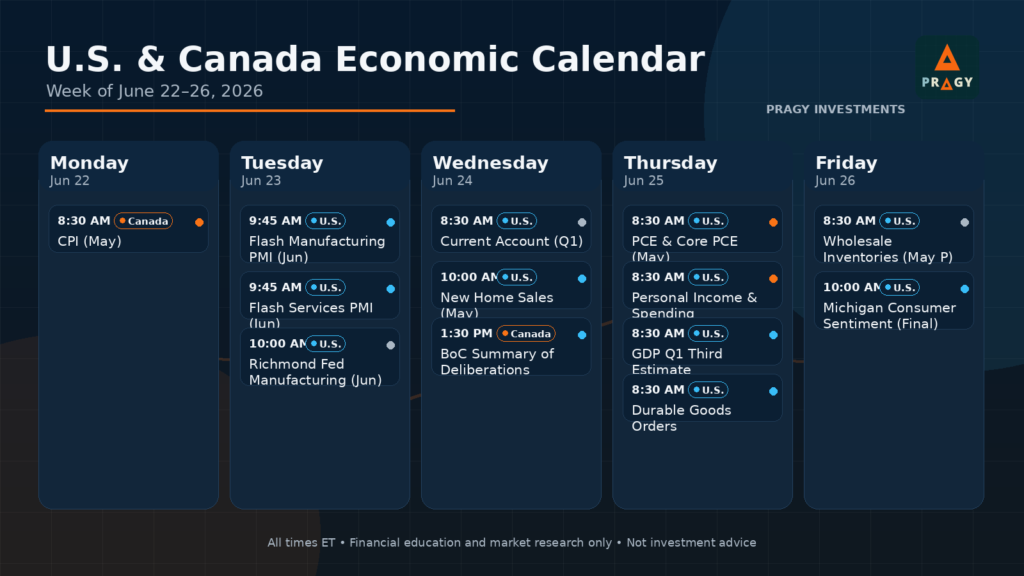

What to Watch Next Week

Next week’s focus is the U.S. and Canada economic calendar for June 22 to June 26. Canada CPI on Monday may influence expectations for the Bank of Canada and Canadian rate-sensitive sectors.

In the U.S., flash PMI data, new home sales, durable goods, Q1 GDP, and personal income and spending will help investors assess whether growth is holding up. The biggest macro focus is likely the May PCE and core PCE data, because inflation remains central to the Federal Reserve outlook.

Markets will also watch whether QQQ leadership continues, whether SPY participation broadens, whether TSX materials stabilize, and whether rate-sensitive sectors can absorb the latest macro data without a larger shift in tone.

Disclaimer

Pragy Investments provides financial education and market research only. This content is not investment advice, financial planning, portfolio management, tax advice, legal advice, or a recommendation to buy, sell, or hold any security. Trading and investing involve risk, including possible loss of capital. Readers are responsible for their own decisions and should consult a qualified financial professional before making financial decisions.